Worked Examples

Examples.RmdExample 1: Random regression with non-Gaussian data

Our first example is the chicken weight data set, already used in the

RTMB Introduction vignette.

We fit the same random regression model, where each chick has its own intercept and slope parameters that are assumed to be normally distributed. However, instead of assuming normal errors, we assume that the observations given the time and chick follow a Box-Cox Cole-Green (BCCG) distribution, which allows for skewness in the data.

data(ChickWeight)

parameters <- list(

mua=0, # Mean slope

log_sda=1, # log-Std of slopes

mub=0, # Mean intercept

log_sdb=1, # log-Std of intercepts

log_sigma=0, # log-Scale of BCCG distribution

nu = 0.1, # Skewness of BCCG distribution

a=rep(0, 50), # Random slope by chick

b=rep(5, 50) # Random intercept by chick

)The joint negative log-likelihood function has the same structure as

in the RTMB vignette, but with the normal likelihood

replaced by the BCCG likelihood, and hence also some necessary parameter

transformations.

nll_chick <- function(parms) {

getAll(ChickWeight, parms, warn=FALSE)

# Optional (enables extra RTMB features)

weight <- OBS(weight)

# Initialise joint negative log likelihood

nll <- 0

# Random slopes

sda <- exp(log_sda); ADREPORT(sda)

nll <- nll - sum(dnorm(a, mean=mua, sd=sda, log=TRUE))

# Random intercepts

sdb <- exp(log_sdb); ADREPORT(sdb)

nll <- nll - sum(dnorm(b, mean=mub, sd=sdb, log=TRUE))

# Data

predWeight <- exp(a[Chick] * Time + b[Chick])

sigma <- exp(log_sigma); ADREPORT(sigma)

nll <- nll - sum(dbccg(weight, mu=predWeight, sigma=sigma, nu=nu, log=TRUE))

# Get predicted weight uncertainties

ADREPORT(predWeight)

# Return

nll

}The model can then again be fitted by constructing the Laplace-approximated marginal log-likelihood function and optimising this using any standard numerical optimiser.

obj_chick <- MakeADFun(nll_chick, parameters, random=c("a", "b"), silent = TRUE)

opt_chick <- nlminb(obj_chick$par, obj_chick$fn, obj_chick$gr)We can use RTMB’s automatic simulation capabilities to

simulate from the fitted model and run a check whether the Laplace

approximation is adequate. All of this is done by a simple call to

checkConsistency().

set.seed(1)

checkConsistency(obj_chick)

#> Parameters used for simulation:

#> mua log_sda mub log_sdb log_sigma nu

#> 0.07799513 -3.86869405 3.80355961 -2.65747574 -2.32420504 3.44873713

#>

#> Test correct simulation (p.value):

#> [1] 0.7383633

#> Simulation appears to be correct

#>

#> Estimated parameter bias:

#> mua log_sda mub log_sdb log_sigma

#> -0.0001346800 0.0064958230 -0.0001147128 -0.0147141495 0.0042912804

#> nu

#> -0.0836398603Lastly, we can also automatically calculate quantile residuals via

probability integral transform using oneStepPredict().

osa_chick <- oneStepPredict(obj_chick, discrete=FALSE, trace=FALSE)

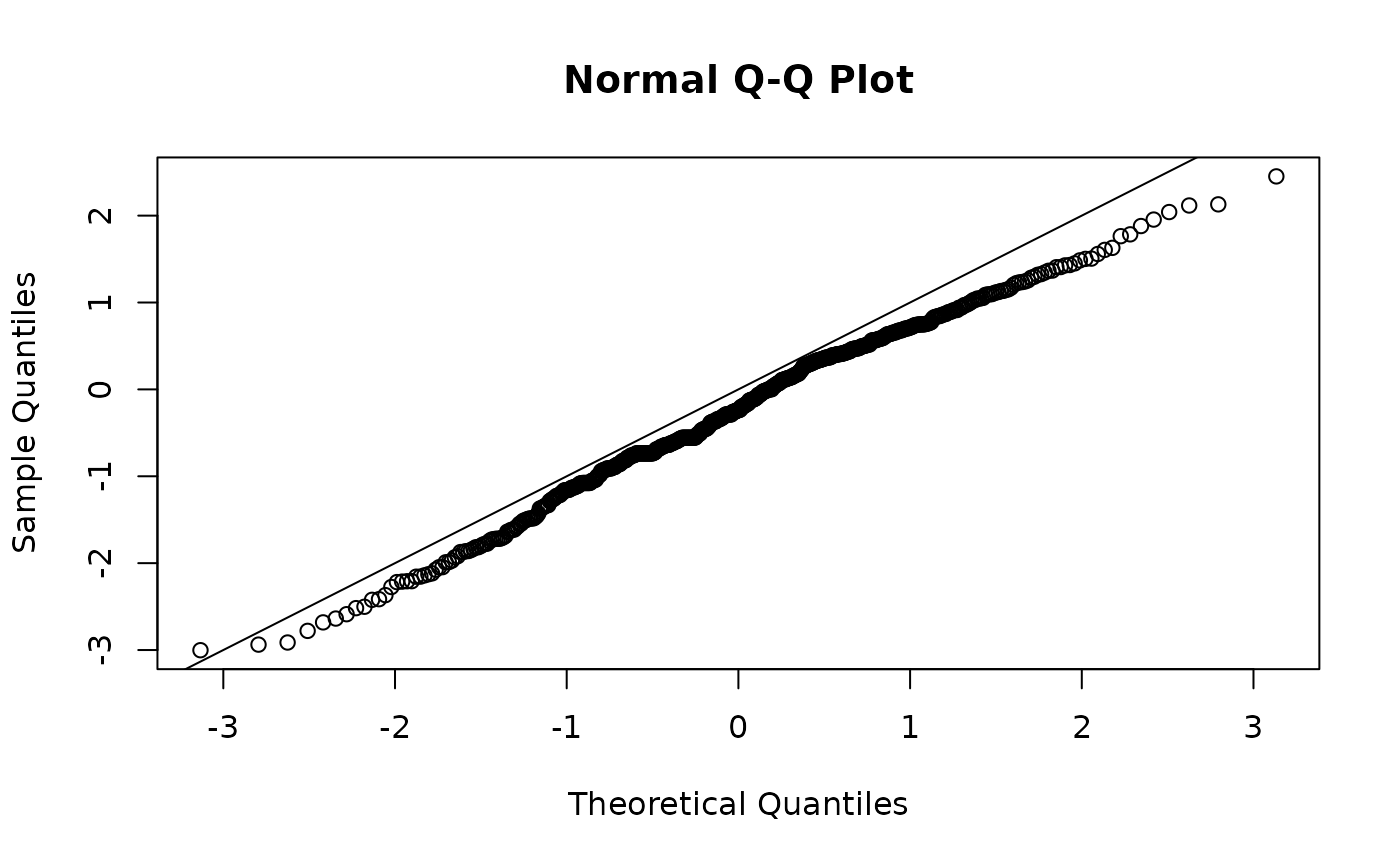

qqnorm(osa_chick$res); abline(0,1)

We see that this model is still not a great fit but a bit better than the Gaussian model.

Example 2: Non-standard random GLM for count data

Our second example is the InsectSprays data set. We will

fit a GLMM where the counts are assumed to follow a generalised

Poisson distribution, allowing for overdispersion (compared to the

standard Poisson distribution). In the model, we simple include a random

effect for each spray type, to account for the fact that some sprays are

more effective than others.

data(InsectSprays)

# Creating the model matrix

X <- model.matrix(~ spray - 1, data = InsectSprays)

par <- list(

beta0 = log(mean(InsectSprays$count)),

beta = rep(0, length(levels(InsectSprays$spray))),

log_phi = log(1),

log_sigma = log(1)

)

dat <- list(

count = InsectSprays$count,

spray = InsectSprays$spray,

X = X

)

nll_insect <- function(par) {

getAll(par, dat, warn=FALSE)

count <- OBS(count)

# Random effect likelihood

sigma <- exp(log_sigma); ADREPORT(sigma)

nll <- - sum(dnorm(beta, 0, sigma, log = TRUE))

# Data likelihood

lambda <- exp(beta0 + as.numeric(X %*% beta)); ADREPORT(lambda)

phi <- exp(log_phi); ADREPORT(phi)

nll <- nll -sum(dgenpois(count, lambda, phi, log = TRUE))

nll

}

obj_insect <- MakeADFun(nll_insect, par, random = "beta", silent = TRUE)

opt_insect <- nlminb(obj_insect$par, obj_insect$fn, obj_insect$gr)

# Checking if the Laplace approximation is adequate

checkConsistency(obj_insect)

#> Parameters used for simulation:

#> beta0 log_phi log_sigma

#> 1.9751913 -3.8913794 -0.2221668

#>

#> Test correct simulation (p.value):

#> [1] 0.605786

#> Simulation appears to be correct

#>

#> Estimated parameter bias:

#> beta0 log_phi log_sigma

#> -0.01672544 0.03395053 -0.00437216

# Check okay

# Calculating quantile residuals

osa_insect <- oneStepPredict(obj_insect, method = "oneStepGeneric",

discrete=TRUE, trace=FALSE)

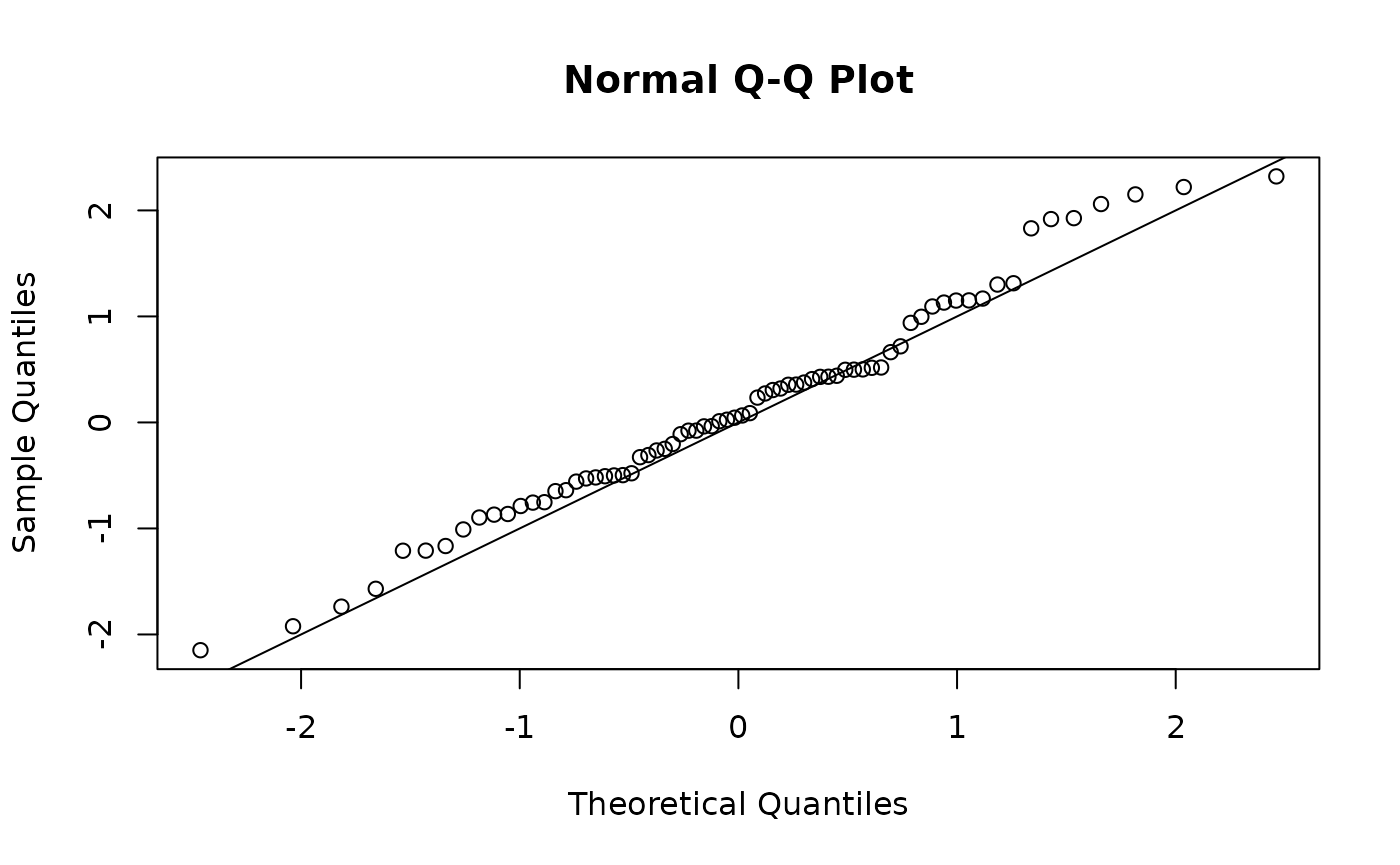

qqnorm(osa_insect$res); abline(0,1)

Example 3: Distributional regression with penalised splines

Our third example covers the dutch boys BMI data set, part of the

gamlss.data package. We will fit a distributional

regression model where the location, scale, and skewness parameters of

the Box-Cox power exponential (BCPE) distribution are modelled as smooth

functions of age using penalised splines. The kurtosis parameter will be

kept constant.

We start by loading packages that are needed.

library(gamlss.data) # Data

library(LaMa) # Creating model matrices

library(Matrix) # Sparse matrices

data(dbbmi)

# Subset (just for speed here)

set.seed(1)

ind <- sample(1:nrow(dbbmi), 2000)

dbbmi <- dbbmi[ind, ]We use the function make_matrices() from package

LaMa to conveniently create design and penalty matrices for

the smooth functions. Internally, this just interfaces

mgcv. The penalty matrix is converted to a sparse matrix

using the Matrix package, to work with RTMB’s

dgmrf() function.

k <- 10 # Basis dimension

modmat <- make_matrices(~ s(age, bs="cs"), data = dbbmi)

X <- modmat$Z # Design matrix

S <- Matrix(modmat$S[[1]], sparse = TRUE) # Sparse penalty matrixThe joint negative log-likelihood function computes covariate

dependent location, scale, and skewness parameters using the design

matrix and regression coefficients. The regression coefficients are

treated as random effects with a multivariate normal distribution with

zero mean and a precision matrix that is a scaled version of the penalty

matrix, which is achieved by calling dgmrf() for each of

them. The scaling/ smoothing parameters are estimated by restricted

maximum likelihood (REML), which is achieved by treating them as

fixed effects and integrating out the regression coefficients and other

fixed effects using the Laplace approximation.

nll_dbbmi <- function(par) {

getAll(par, dat, warn=FALSE)

bmi <- OBS(bmi)

# Calculating response parameters

mu <- exp(X %*% c(beta0_mu, beta_age_mu)); ADREPORT(mu) # Location

sigma <- exp(X %*% c(beta0_sigma, beta_age_sigma)); ADREPORT(sigma) # Scale

nu <- X %*% c(beta0_nu, beta_age_nu); ADREPORT(nu) # Skewness

tau <- exp(log_tau); ADREPORT(tau) # Kurtosis

# Data likelihood: Box-Cox power exponential distribution

nll <- - sum(dbcpe(bmi, mu, sigma, nu, tau, log=TRUE))

# Penalised splines as random effects: log likelihood / penalty

lambda <- exp(log_lambda); REPORT(lambda)

nll <- nll - dgmrf(beta_age_mu, 0, lambda[1] * S, log=TRUE)

nll <- nll - dgmrf(beta_age_sigma, 0, lambda[2] * S, log=TRUE)

nll <- nll - dgmrf(beta_age_nu, 0, lambda[3] * S, log=TRUE)

nll

}

par <- list(

beta0_mu = log(18), beta0_sigma = log(0.15),

beta0_nu = -1, beta_age_mu = rep(0, k-1),

beta_age_sigma = rep(0, k-1), beta_age_nu = rep(0, k-1),

log_tau = log(2),

log_lambda = log(rep(1e4, 3))

)

dat <- list(

bmi = dbbmi$bmi,

age = dbbmi$age,

X = X,

S = S

)As we are using REML, we are integrating out all parameters

that are not smoothing parameters log_lambda. The model is

then fitted by constructing the Laplace-approximated restricted

log-likelihood function and optimising this.

# Restricted maximum likelihood (REML) - also integrating out fixed effects

random <- names(par)[names(par) != "log_lambda"]

obj_dbbmi <- MakeADFun(nll_dbbmi, par, random = random, silent = TRUE)

opt_dbbmi <- nlminb(obj_dbbmi$par, obj_dbbmi$fn, obj_dbbmi$gr)We can have access to all ADREPORT()ed quantities and

their standard deviation using sdreport().

sdr <- sdreport(obj_dbbmi, ignore.parm.uncertainty = TRUE)

par <- as.list(sdr, "Est", report = TRUE)

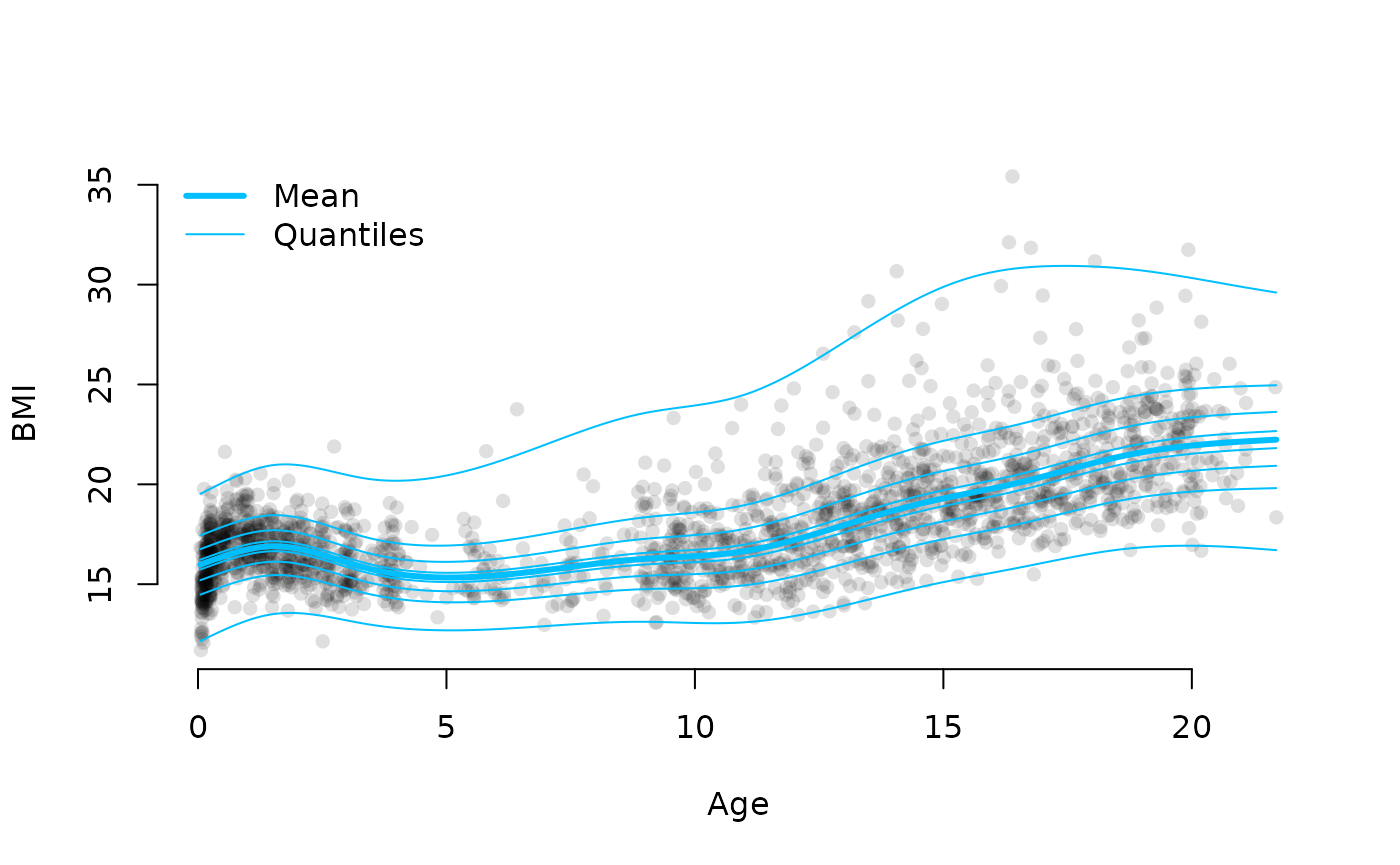

par_sd <- as.list(sdr, "Std", report = TRUE)This way, we can easily plot the estimated smooth functions with confidence intervals and the conditional distribution of BMI given age.

age <- dbbmi$age

ord <- order(age)

# Plotting estimated effects

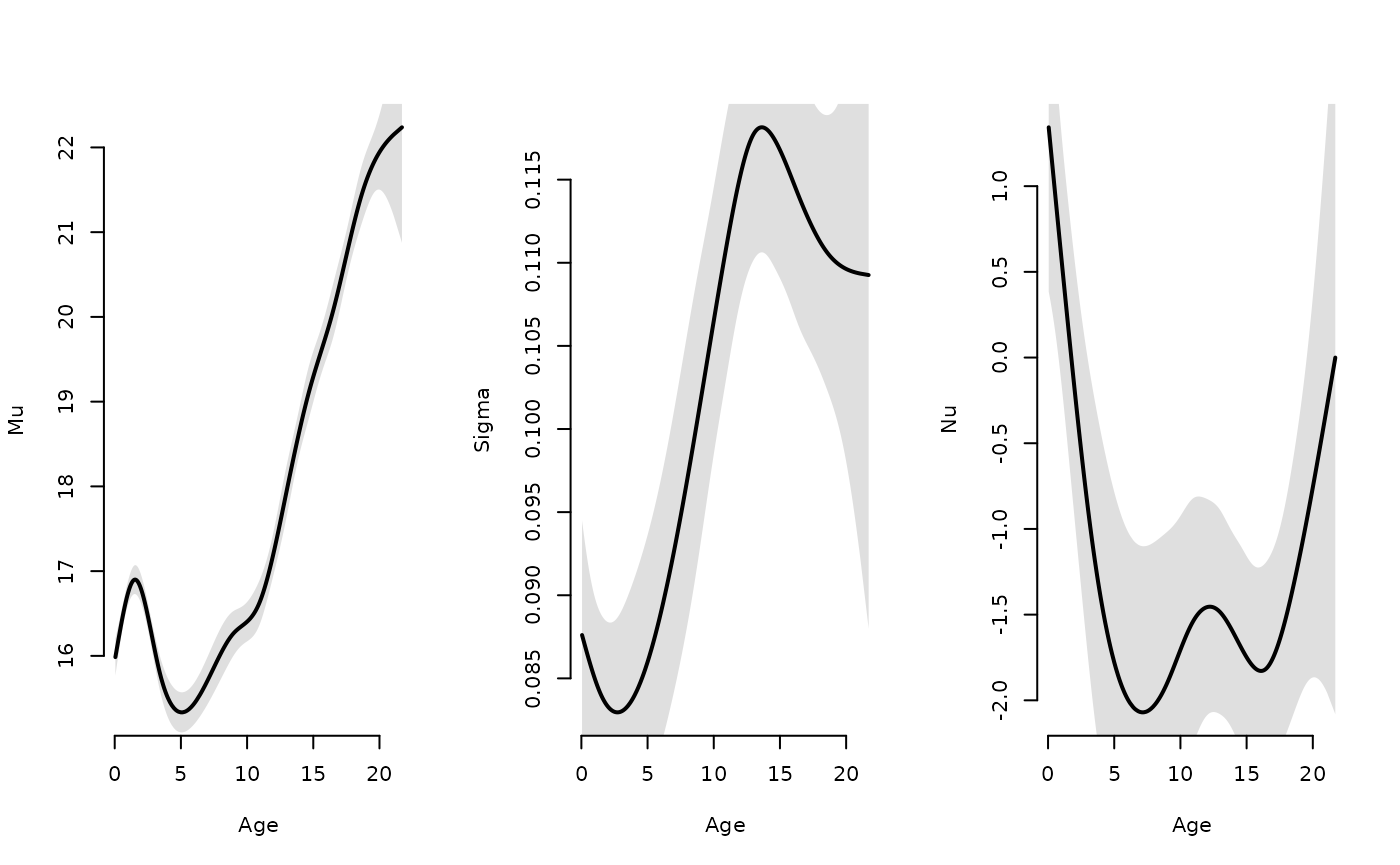

oldpar <- par(mfrow = c(1,3))

plot(age[ord], par$mu[ord], type = "l", lwd = 2, bty = "n", xlab = "Age", ylab = "Mu")

polygon(c(age[ord], rev(age[ord])),

c(par$mu[ord] + 2*par_sd$mu[ord], rev(par$mu[ord] - 2*par_sd$mu[ord])),

col = "#00000020", border = "NA")

plot(age[ord], par$sigma[ord], type = "l", lwd = 2, bty = "n", xlab = "Age", ylab = "Sigma")

polygon(c(age[ord], rev(age[ord])),

c(par$sigma[ord] + 2*par_sd$sigma[ord], rev(par$sigma[ord] - 2*par_sd$sigma[ord])),

col = "#00000020", border = "NA")

plot(age[ord], par$nu[ord], type = "l", lwd = 2, bty = "n", xlab = "Age", ylab = "Nu")

polygon(c(age[ord], rev(age[ord])),

c(par$nu[ord] + 2*par_sd$nu[ord], rev(par$nu[ord] - 2*par_sd$nu[ord])),

col = "#00000020", border = "NA")

par(oldpar)

# Plotting conditional distribution

plot(dbbmi$age, dbbmi$bmi, pch = 16, col = "#00000020",

xlab = "Age", ylab = "BMI", bty = "n")

lines(age[ord], par$mu[ord], lwd = 3, col = "deepskyblue")

# Compute quantiles (point estimates)

par <- lapply(par, as.numeric)

ps <- seq(0, 1, length = 8)

ps[1] <- 0.005 # avoid 0 and 1

ps[length(ps)] <- 0.995 # avoid 0 and 1

for(p in ps) {

q <- qbcpe(p, par$mu, par$sigma, par$nu, par$tau) # quantiles

lines(age[ord], q[ord], col = "deepskyblue")

}

legend("topleft", lwd = c(3, 1), col = "deepskyblue", legend = c("Mean", "Quantiles"), bty = "n")

Example 4: Zero inflation

In this example, we look at the aep data set, containing

data on the number of inappropriate days spent in the hospital and the

length of a stay for patients admitted to a hospital in Barcelona. These

data have been analysed by Gange et al. (1996). They fitted a binomial

logistic regression model as well as a beta-binomial regression model,

concluding that the beta-binomial model produced a better fit. Due to

the large number of zeros in the data, we will here also fit a

zero-inflated binomial model and compare the results.

library(gamlss.data)

head(aep)

#> los noinap loglos sex ward year age y.noinap y.failures

#> 1 15 0 0.4054651 2 2 88 0 0 15

#> 2 42 20 1.4350845 2 1 88 18 20 22

#> 3 8 6 -0.2231436 1 1 88 19 6 2

#> 4 9 6 -0.1053605 1 2 88 23 6 3

#> 5 7 0 -0.3566749 1 2 88 2 0 7

#> 6 10 2 0.0000000 2 2 88 -8 2 8We start by fitting the 2 binomial models. We only define one likelihood function and fix the zero probability to 0 for the binomial model.

# Defininig the model matrix for the model reported in Gange et al. (1996)

X <- model.matrix(~ age + ward + loglos * year, data = aep)

# (zero-inflated) binomial likelihood

nll_aep <- function(par) {

getAll(par, dat)

y <- OBS(y); size <- OBS(size)

prob <- plogis(X %*% beta); ADREPORT(prob) # linear predictor and link

zeroprob <- plogis(logit_zeroprob); ADREPORT(zeroprob)

- sum(dzibinom(y, size, prob, zeroprob, log = TRUE))

}

# Initial parameters

beta_init <- c(-1, rep(0, ncol(X)-1))

names(beta_init) <- colnames(X)

par <- list(beta = beta_init)

dat <- list(

y = aep$y[,1],

size = aep$los,

X = X

)

# Fitting the binomial model (zeroprob fixed at 0)

map <- list(logit_zeroprob = factor(NA)) # fixing at initial value

par$logit_zeroprob <- qlogis(0) # set to zero

obj_aep1 <- MakeADFun(nll_aep, par, silent = TRUE, map = map)

opt_aep1 <- nlminb(obj_aep1$par, obj_aep1$fn, obj_aep1$gr)

# Fitting the zero-inflated binomial model, no parameter restrictions

par$logit_zeroprob <- qlogis(1e-2) # more sensible initial value

obj_aep2 <- MakeADFun(nll_aep, par, silent = TRUE)

opt_aep2 <- nlminb(obj_aep2$par, obj_aep2$fn, obj_aep2$gr)

#> Warning in nlminb(obj_aep2$par, obj_aep2$fn, obj_aep2$gr): NA/NaN function

#> evaluation

# Reporting

sdr_aep1 <- sdreport(obj_aep1)

sdr_aep2 <- sdreport(obj_aep2)

beta1 <- as.list(sdr_aep1, "Est")$beta

beta2 <- as.list(sdr_aep2, "Est")$beta

(zeroprob2 <- as.list(sdr_aep2, "Est", report = TRUE)$zeroprob)

#> [1] 0.4294577

round(rbind(beta1, beta2), 3)

#> (Intercept) age ward2 ward3 loglos year90 loglos:year90

#> beta1 -1.006 0.006 -0.468 -0.615 0.518 0.168 -0.204

#> beta2 0.058 0.009 -0.622 -0.873 0.235 -0.294 -0.087We find that accounting for the zero-inflation somewhat changes the estimated coefficients. Now we also fit the beta-binomial model. In this model, the shape parameters are modelled as p_i / \theta_i and (1-p_i) / \theta_i, where p_i is the covariate-dependent probability for observation i and \theta_i is a parameter controlling the overdispersion. The parameter \theta_i is modelled as a function of year only, exactly as in Gange et al. (1996).

# Beta-binomial likelihood

nll_aep2 <- function(par) {

getAll(par, dat)

y <- OBS(y); size <- OBS(size)

theta <- plogis(X_theta %*% beta_theta); ADREPORT(theta) # overdispersion parameter

prob <- plogis(X %*% beta); ADREPORT(prob) # linear predictor and link

- sum(dbetabinom(y, size, prob / theta, (1-prob) / theta, log = TRUE))

}

# Design matrices

X <- model.matrix(~ ward + loglos + year, data = aep)

X_theta <- model.matrix(~ year, data = aep)

# Initial parameters

beta <- c(-1, rep(0, ncol(X)-1)); names(beta) <- colnames(X)

beta_theta <- c(1, 0); names(beta_theta) <- colnames(X_theta)

par <- list(beta = beta, beta_theta = beta_theta)

dat <- list(

y = aep$y[,1],

size = aep$los,

X = X,

X_theta = X_theta

)

obj_aep3 <- MakeADFun(nll_aep2, par, silent = TRUE)

opt_aep3 <- nlminb(obj_aep3$par, obj_aep3$fn, obj_aep3$gr)

sdr_aep3 <- sdreport(obj_aep3)

beta3 <- as.list(sdr_aep3, "Est")$beta

round(beta3, 3)

#> (Intercept) ward2 ward3 loglos year90

#> -1.126 -0.320 -0.606 0.537 0.295Example 5: Copulas

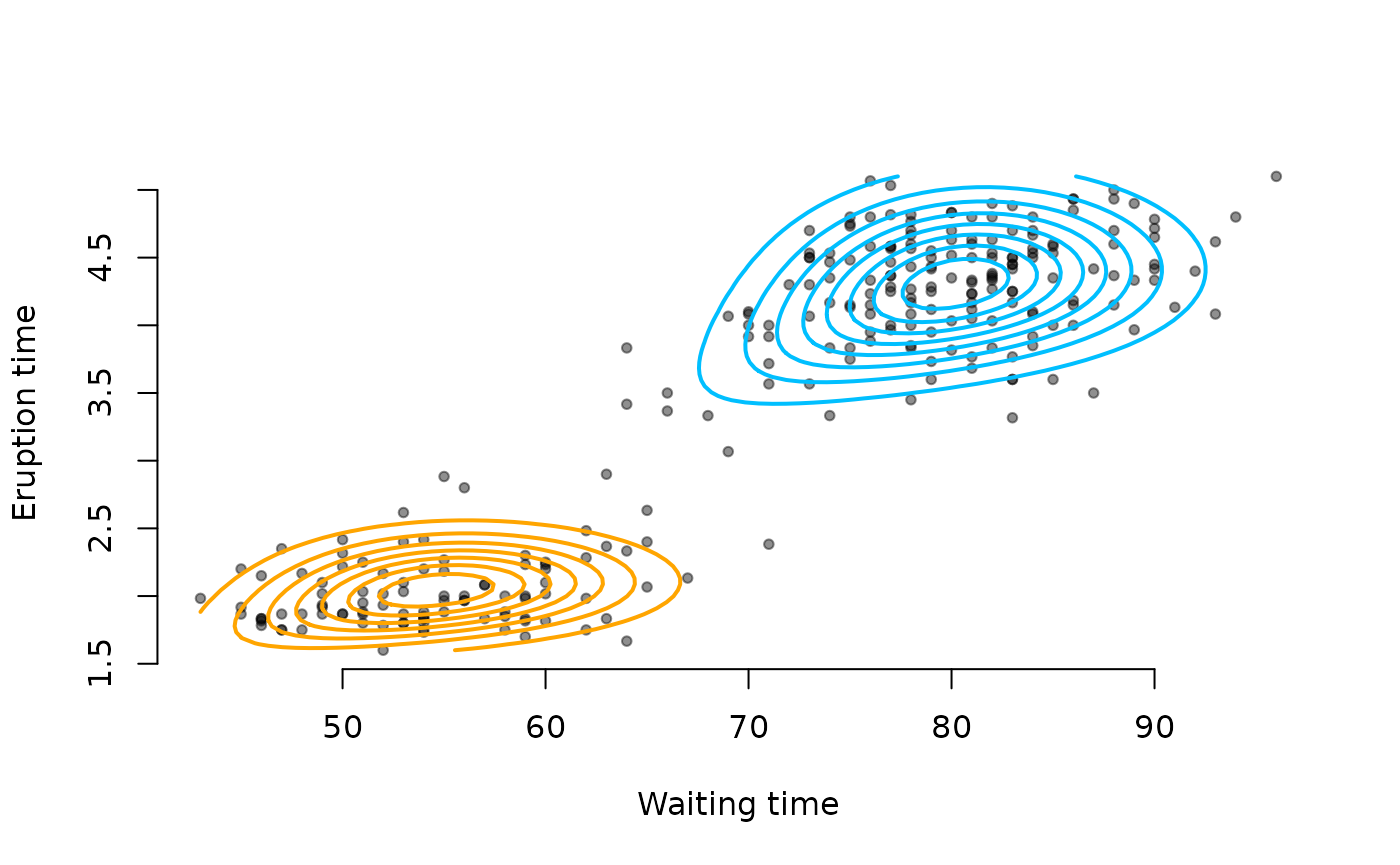

For this example, we are modelling the faithful data

set. It contains measurements of the waiting time between eruptions and

the duration of the eruption for the Old Faithful geyser in Yellowstone

National Park, Wyoming, USA. We will fit a mixture of two bivariate

distributions, where each component has normal marginal distributions

and a Clayton copula to model the dependence between the two

variables.

data(faithful)Specifying the mixture likelihood using dcopula() and

cclayton() for the components is straightforward, it’s just

imporant to not confuse mixture components and dimensions.

nll_copula <- function(par) {

getAll(par, faithful)

REPORT(mu1); REPORT(mu2)

sigma1 <- exp(log_sigma1); REPORT(sigma1) # marginal sds component 1

sigma2 <- exp(log_sigma2); REPORT(sigma2) # marginal sds component 2

theta <- exp(log_theta); REPORT(theta) # dependence parameters

alpha <- exp(log_alpha); REPORT(alpha) # mixture weights

# Marginal densities

# Margin 1: Waiting

d1 <- cbind(dnorm(waiting, mu1[1], sigma1[1], log=TRUE), # Component 1

dnorm(waiting, mu2[1], sigma2[1], log=TRUE)) # Component 2

# Margin 2: Eruptions

d2 <- cbind(dnorm(eruptions, mu1[2], sigma1[2], log=TRUE), # Component 1

dnorm(eruptions, mu2[2], sigma2[2], log=TRUE)) # Component 2

# Marginal CDFs

# Margin 1: Waiting

p1 <- cbind(pnorm(waiting, mu1[1], sigma1[1]), # Component 1

pnorm(waiting, mu2[1], sigma2[1])) # Component 2

# Margin 2: Eruptions

p2 <- cbind(pnorm(eruptions, mu1[2], sigma1[2]), # component 1

pnorm(eruptions, mu2[2], sigma2[2])) # component 2

# Computing mixture likelihood:

ll1 <- dcopula(d1[,1], d2[,1], p1[,1], p2[,1], cclayton(theta[1]), log=TRUE) # f1(x,y)

ll2 <- dcopula(d1[,2], d2[,2], p1[,2], p2[,2], cclayton(theta[2]), log=TRUE) # f2(x,y)

# alpha * f1(x,y) + (1-alpha) * f2(x,y) on log scale for each obervation

ll <- logspace_add(log_alpha + ll1, log1p(-alpha) + ll2)

- sum(ll) # returning negative sum

}We fit the model as usual, now using reporting to easily extract the estimated parameters on their natural scale:

# Initial parameters

par <- list(

mu1 = c(55, 2), mu2 = c(80, 4),

log_sigma1 = log(c(10, 1)), log_sigma2 = log(c(10, 1)),

log_theta = log(c(0.5, 0.5)),

log_alpha = log(0.5)

)

obj_copula <- MakeADFun(nll_copula, par, silent = TRUE)

opt_copula <- nlminb(obj_copula$par, obj_copula$fn, obj_copula$gr)

mod_copula <- obj_copula$report()

# Extract transformed parameters

mu1 <- mod_copula$mu1

mu2 <- mod_copula$mu2

sigma1 <- mod_copula$sigma1

sigma2 <- mod_copula$sigma2

theta <- mod_copula$theta

alpha <- mod_copula$alphaWe can plot the result:

# Scatterplot

plot(faithful$waiting, faithful$eruptions, pch = 20, bty = "n",

xlab = "Waiting time", ylab = "Eruption time", col = "#00000070")

# Grid for evaluation

xseq <- seq(min(faithful$waiting), max(faithful$waiting), length.out = 80)

yseq <- seq(min(faithful$eruptions), max(faithful$eruptions), length.out = 80)

# Evaluate component densities on grid

f1 <- outer(xseq, yseq, function(x,y){

d1c1 <- dnorm(x, mu1[1], sigma1[1])

d2c1 <- dnorm(y, mu1[2], sigma1[2])

p1c1 <- pnorm(x, mu1[1], sigma1[1])

p2c1 <- pnorm(y, mu1[2], sigma1[2])

dcopula(d1c1, d2c1, p1c1, p2c1, cclayton(theta[1]))

})

f2 <- outer(xseq, yseq, function(x,y){

d1c2 <- dnorm(x, mu2[1], sigma2[1])

d2c2 <- dnorm(y, mu2[2], sigma2[2])

p1c2 <- pnorm(x, mu2[1], sigma2[1])

p2c2 <- pnorm(y, mu2[2], sigma2[2])

dcopula(d1c2, d2c2, p1c2, p2c2, cclayton(theta[2]))

})

# Add contours

contour(xseq, yseq, alpha * f1, add = TRUE, nlevels = 8,

drawlabels = FALSE, col = "orange", lwd = 2)

contour(xseq, yseq, (1-alpha) * f2, add = TRUE, nlevels = 8,

drawlabels = FALSE, col = "deepskyblue", lwd = 2)

Example 6: Multivariate stochastic volatility

This example reproduces one of the TMB examples. It fits

a multivariate stochastic volatility model to financial returns data. In

the example given here,

the response distribution is a multivariate Gaussian, with the marginal

variance for each of the three time series being time-varying and

modelled based on a latent volatility process. We generalise the example

to a multivariate t distribution, which typically results in a better

fit to financial returns data, due to the heavier tails.

We get the data from

source("https://raw.githubusercontent.com/kaskr/RTMB/master/tmb_examples/sdv_multi_data.R")The code below is basically the same as in the original example, but

uses a multivariate t distribution (dmvt()) in the data

likelihood. Note that the Cov matrix is now not actually

the covariance matrix anymore, but only proportional to it.

# Multivatiate SV model from Table 5 of Skaug and Yu "A flexible and automated likelihood based

# framework for inference in stochastic volatility models." Computational Statistics & Data Analysis 76 (2014): 642-654.

## Parameter initial guess

par <- list(

logit_phi = qlogis(rep(0.97,p)), # See eqn (12) in Skaug and Yu (2014)

log_sigma = log(rep(0.2,p)), # ---------||---------

mu_y = rep(-0.5,p), # ---------||---------

off_diag_x = rep(0,p), # ---------||---------

h = matrix(0,nrow=n,ncol=p), # ---------||---------

log_df = log(20) # this allows for heavier tails

)

# Negative joint likelihood (nll) of data and parameters

nll_svt <- function(par) {

getAll(par)

# Optionally mark the observation object

y <- OBS(y)

# Parameters on natural scale

sigma <- exp(log_sigma)

phi <- plogis(logit_phi)

sigma_init <- sigma / sqrt(1-phi^2)

df <- exp(log_df)

nll <- 0 # Start collecting contributions

# Prior on state variable (h)

nll <- nll - sum(dnorm(h[1,], 0, sigma_init, log=TRUE)) # Start in stationary distribution

for(j in 1:p) {

nll <- nll - sum(dnorm(h[-1,j], phi[j]*h[-n,j], sigma[j], log=TRUE)) # AR(1) process for each dimension

}

# Parameterizes correlation matrix of X in terms of Cholesky factor

L <- diag(p)

L[lower.tri(L)] <- off_diag_x

row_norms <- apply(L, 1, function(row) sqrt(sum(row^2)))

L <- L / row_norms

R <- L %*% t(L) # Correlation matrix of X (guarantied positive definite)

# Likelihood of data y given h

for(i in 1:n){

sigma_y <- exp(0.5 * (mu_y + h[i,])) # variance depending on state

Cov <- diag(sigma_y) %*% R %*% diag(sigma_y)

nll <- nll - sum(dmvt(y[i,], 0, Cov, df, log = TRUE))

}

nll

}

obj_svt <- MakeADFun(nll_svt, par, random="h", silent = TRUE)

system.time(

opt_svt <- nlminb(obj_svt$par, obj_svt$fn, obj_svt$gr)

)

#> user system elapsed

#> 14.192 0.025 14.217

rep <- sdreport(obj_svt)

rep

#> sdreport(.) result

#> Estimate Std. Error

#> logit_phi 3.6269542 0.49413568

#> logit_phi 3.1290137 0.38240912

#> logit_phi 4.7269255 0.80777552

#> log_sigma -1.9420595 0.21824559

#> log_sigma -2.0048373 0.17178092

#> log_sigma -2.4015626 0.34312782

#> mu_y -1.1388822 0.18663075

#> mu_y -1.0938327 0.11876150

#> mu_y -1.5630285 0.31299779

#> off_diag_x -1.3641053 0.06465394

#> off_diag_x -1.1315426 0.06265752

#> off_diag_x 0.7446955 0.04688460

#> log_df 1.9632807 0.13715707

#> Maximum gradient component: 0.0009298738